prediction markets: the next level

disclaimers: this article assumes familiarity with prediction markets and their current implementations. my views are my own, not those of my employer. i am founding engineer at gondor.fi, a startup currently working on the technology discussed in this piece.

introduction

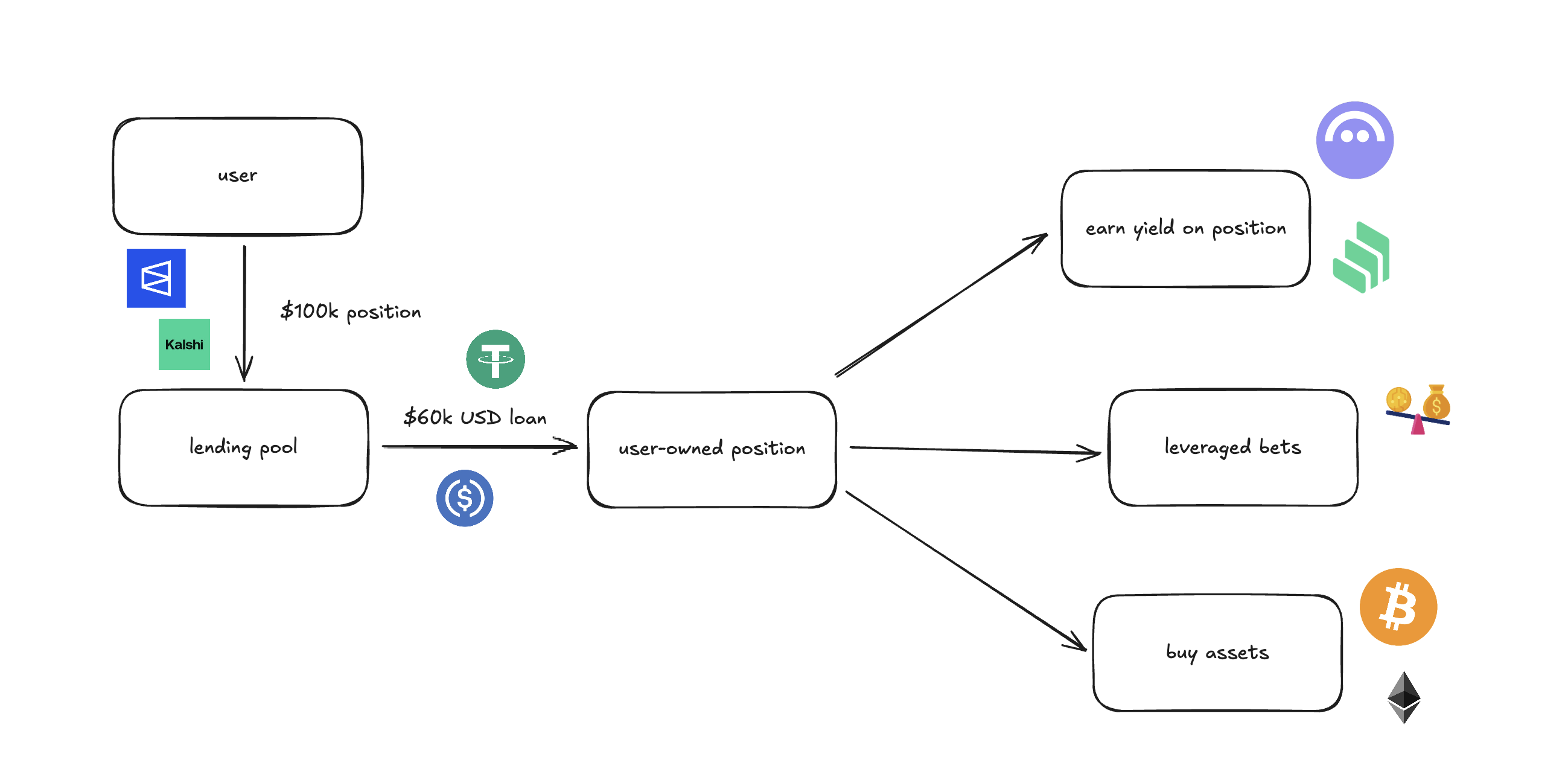

prediction markets today are powerful information engines, but they "sink" your capital – money cannot flow out without selling the position. this article discusses a new primitive built on top of prediction markets with the goal of solving the current issues with prediction markets: collateralizing and borrowing against your prediction market positions.

the problem

it is january 1st, 2026. you are extremely confident that taylor swift will be the top streamed spotify artist by the end of the year, for whatever reason. maybe you've done an in-depth analysis of music and spotify trends and have hard data to back your position. maybe you are convinced her new album will blow up. maybe you're just a giant swiftie. the market is giving you a chance to buy shares on her being #1 for 30c (implying a 30% probability), so you buy $10000 worth of shares.

the issue: $10000 of your money is now locked up until december 31, 2026. you will have to sell a part of your position if you need any cash in the short-term. you would likely be taxed on any profit you made.

the concept and problems it solves

what if you were able to borrow $5000 against this position? that way, you would be able to pay any short-term capital costs, without having to reduce any of your position. you can wait until the end of 2026 and comfortably pay back your loan from your profits, while keeping a pretty solid amount for yourself!1

this is the next level of prediction markets -- unlocking the ability to turn your positions and information into a line of credit.

-

increases and incentivizes liquidity

it's a well-known phenomenon that the liquidity of borrowing directly impacts the liquidity of a market2. many long-term markets i.e. markets that expire in more than 6 months tend to have poorer liquidity than their shorter-term counterparts, owing to the opportunity risk of traders locking up their capital for multiple months at a time. market makers (who provide liquidity in most mature markets) also are often in requirement of short-term capital to adjust positions, and being able to borrow against their more liquid, longer-term positions can help them have free cash to fund shorter-term positions. -

corrects mispricings and incentivizes arbitrage

several markets, even major ones, are mispriced due to longshot bias3 and also due simply to low volumes or market inefficiency i.e. a popular one was The Second Coming of Christ in 2025 being priced at roughly 3-4% probability of occurring. the bet can best be understood as a bet on Polymarket changing the resolution criteria of the event4, and its pricing can be understood as a market failure i.e. locking up capital until the end of 2025 for a return of 4.1%, barely crossing the risk-free rate of return5 is -EV for market participants. however, combining this position and several others with similar criteria could yield a close to 10-12% return with minimal risk, assuming interest costs are low.6 -

composability

prediction markets are currently isolated from the rest of the financial ecosystem, crypto or otherwise – the ability to collateralize them, especially on-chain, can have significant mutually beneficial positive externalities. collateralized positions can have a lot of interesting applications, including using them to earn yield, and providing a venue for external capital to gain exposure to prediction markets by lending to borrowers.

considerations and issues

-

implementation-specific: liquidations, pricing, collateral choice

if a news announcement would lead to the direct closure of a market, one of its shares is likely to drop to zero almost immediately – liquidation on these positions in these kinds of markets is extremely difficult, and would require careful monitoring, risk management and constant adjustments for volatility and diversification of positions.

pricing these positions is also an extremely delicate task – prices need to be constantly accurate, the orderbook must be deep enough to use the best price, the position size must be taken into account and much more. most prediction markets are centralized infrastructure, and an outage or any corruption in their API data could cause explosive damage, especially with composable ecosystems. -

general issues

binary options are notoriously difficult to hedge – while prediction markets are excellent hedging tools for price exposure to equities and commodities in the face of real-world events, prediction market positions themselves are near-impossible to hedge. how do you hedge an asset whose counter-asset is a direct mirror of its own price, and with no continuous outcomes ($1 or $0 on settlement)?.

this issue magnifies when leverage and composability is enabled – without proper risk management from both traders and protocols that enable leverage and borrowing, a liquidation cascade could be triggered leading to massive losses and if liquidations are not quick enough, leave lending protocols in bad debt.

conclusion

if this article interested you and you think you can contribute to fixing both implementation-specific and general issues with prediction markets, you should join us at gondor. we're building the DeFi layer for prediction markets, and collateralization is only the beginning of our plans. email us at join@gondor.fi!

if you just want to chat, shoot me an email at kesh.ramamurthy@gmail.com.

footnotes

- this assumes price action doesn't fall by much during 2026 – we'll come to this later.

- Brunnermeier, Markus Konrad and Pedersen, Lasse Heje, Market Liquidity and Funding Liquidity (June 2009). The Review of Financial Studies, Vol. 22, Issue 6, pp. 2201-2238, 2009, Available at SSRN: https://ssrn.com/abstract=1408432 or http://dx.doi.org/hhn098

- https://en.wikipedia.org/wiki/Favourite-longshot_bias

- i am sure some flow is due to believers in the second coming…

- 4.06% on a 10-year T-bond, at the time of writing.

- which they likely would be, given the risk to lenders is minimal.